NGA Government Relations

NGA works to ensure that Governors’ views are represented in shaping federal policy by maintaining regular contact with congressional leaders and key administration officials, keeping up-to-date information on critical state–federal issues and coordinating state action.

We work closely with Governors’ Washington, D.C., office representatives, state-federal contacts and other state and local government organizations to maximize the effectiveness of NGA’s lobbying activities. Specifically, our staff serve as policy experts and liaisons to Congress and executive branch agencies and coordinate the work and policy activities of NGA task forces.

Governors believe federal action should be limited to the powers expressly conveyed by the Constitution, to preserve state sovereignty in legislative and regulatory matters the Executive Committee has added the following bipartisan priorities:

- Enhancing emergency management;

- Streamlining permitting processes;

- Supporting flexibility and waiver opportunities and funding for state and territorial designed Medicaid, SNAP, and TANF;

- Ensuring the federal government meets its already committed obligations for federally funded projects across states, territories and Commonwealths.

Additional federal priorities have been developed by each of NGA’s Governor-led Task Forces and can be found on the Task Force pages below.

NGA Task Forces & Council of Governors

- Education, Workforce and Community Investment Task Force

- Economic Development and Revitalization Task Force

- Public Health and Emergency Management Task Force

- Council Of Governors

Advocacy Communications Library

NGA Reaffirms Commitment to State Authority Over Elections

NGA Joins Coalition Letter Urging Passage of the Water Resources Development Act

NGA Statement on Election Integrity

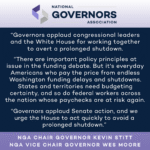

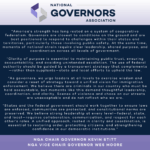

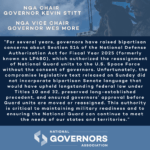

Governors Applaud Senate Action to Avoid Shutdown

Statement from the National Governors Association

Statement from NGA Chair and Vice Chair

Local, State Coalition Presses Congress for Urgent SNAP Fix

NGA Joins Coalition Letter Outlining SNAP Recommendations

NGA Sends Letter to Congress on National Guard Authority

Public Health and Emergency Management Task Force Sends Letter on FEMA Act

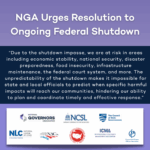

NGA Urges Resolution to Ongoing Federal Shutdown